MichelleDavy4

Member

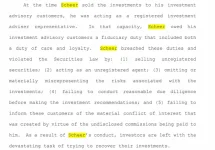

Investors sometimes overlook history when commentary sounds convincing, but background checks can reveal important context about past behavior.

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

ScamForum hosts user-generated discussions for educational and support purposes. Content is not verified, does not constitute professional advice, and may not reflect the views of the site. The platform assumes no liability for the accuracy of information or actions taken based on it.