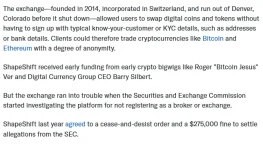

I’ve been reading up on ShapeShift.com and the discussion around its no‑KYC model and regulatory reactions, and I wanted to share what I’ve found and see how people here interpret it. From what I can tell based on public information, ShapeShift started as a cryptocurrency exchange that didn’t require users to go through KYC or identity checks, which was a big part of its appeal for privacy‑minded traders. At one point, the company moved to a decentralized model that routed users to decentralized exchange protocols instead of acting as the counterparty itself, and this change was explicitly tied to ending the KYC requirement because the platform no longer directly transacted with users under its old model.

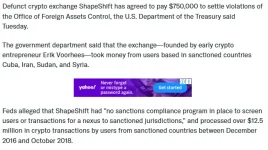

There have also been notable regulatory interactions. ShapeShift AG, a version of the exchange that operated prior to its decentralization, settled with the U.S. Office of Foreign Assets Control for apparent sanctions violations related to users in countries subject to sanctions, with a $750,000 settlement reported. Prior to that, the platform faced scrutiny from the SEC over registration and securities issues, and it made changes to its structure over time.

At the same time, the platform has continued to evolve, with more recent moves integrating privacy‑focused features like shielded Zcash transactions, and updates to its DAO‑governed, self‑custodial architecture supporting decentralized trading across multiple blockchains. There are also mixed public user impressions in reviews, with some users praising ease of use and others reporting support issues and frustration. So I’m curious how people here see the trajectory of ShapeShift given all this: does its history suggest anything about the broader challenges of non‑custodial, no‑KYC crypto tools? Has the shift to decentralized protocols made a meaningful difference in how regulators view it? And how do you reconcile the privacy‑focused ethos with evolving compliance expectations?